On January 26, I wrote an article, To ensure the future of the U.S. racing industry, the betting business has to change. Today, I will expand on the discussion on Advance Deposit Wagering (ADW) numbers, particularly due to the significant handle changes.

I would like to look once more at the chart below, which was discussed in that earlier article. At first glance, given the cancellations and postponements of race meetings, almost all that did race did so without customers. While live track handle is only 10-15 percent of the total handle, on-track handle is two to three times more profitable for the track and for the purse account.

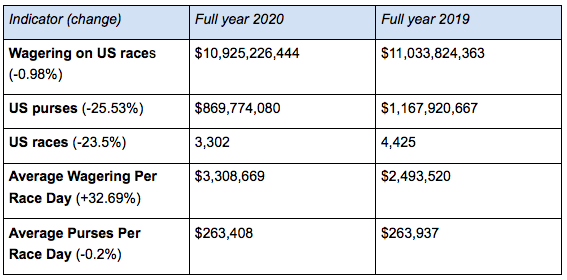

U.S. RACES, WAGERING AND PURSES - 2020 vs 2019

While the full-year handle in 2020 was fortunately less than one percent down on 2019, the total purses paid were down 25 percent, and the number of races down a similar percentage. However, the 2020 purses were already budgeted and paid for. The money earned from wagering on these races is for future use.

As we will see below, the four top ADW companies (TVG, Churchill Downs, Xpressbet and NYRA Bets) all had handle increases for 2020 that were 50-100 percent greater than the handle in 2019.

With very little on-track handle in 2020, the ADW wagering was very strong, but the contribution to purses was significantly less in 2020. This is because the contribution to purses from ADW wagering is less than half of what is paid from an on-track wager. While the wagering in total in 2020 was strong thanks to ADWs, the payments to purses and to the racetracks were down significantly.

So, despite decent handle for 2020, the tracks did not reach the level of revenue consistent with the same wagering in 2019. Many tracks must also have paid out to purses in 2020 more than they had earned as no one anticipated a pandemic that drove ADWs to record levels as track revenues and purses declined.

While the wagering handle was very stable for the full year, there were many dramatic monthly shifts. The professional sports world in America just stopped (MLB, NBA, NHL, PGA and all collegiate sports) from March until well into the summer, and the PGA was the first sport back - in June. For most of late March, April and May, racing had an opportunity to promote itself, and I think the industry responded.

Horse Racing Nation listed the top ten tracks with the highest handle increase for 2020 in its January 4 issue. The top five tracks were really the only ones running in late March, April and May:

- Gulfstream Park handle grew by over $450 million, a 30 percent increase over 2019 while running 100 fewer races.

- Tampa Bay Downs had a 50 percent increase of $170,679,321 over 2019 with 20 percent more races.

- Oaklawn Park had a handle increase of 63% (or $147 million) over 2019 on the same number of races and an increased average field size from 9.1 to 9.7 horses per race.

- Will Rogers Downs handle grew by over $114 million for an amazing 679 percent increase over 2019.

- Fonner Park handle increased from $7.5 million in 2019 to $100 million in 2020.

Some of these increases can be directly attributed to the television broadcasts by Fox Sports, TVG, NBCSN, and MSG and supported by New York Racing Association, Churchill Downs, the Breeders’ Cup, the Jockey Club and America’s Day at the Races.

However, putting these handle increases in context, these five tracks alone, including two that most handicappers east of the Mississippi had never placed a bet on, had a grand total handle increase of $987 million. That number is around 9.1 percent of the total handle wagered in the U.S. in 2020.

Congratulations are due to the management teams that kept these tracks up and operating during the pandemic. No professional or college sports teams were playing at this time and major tracks such as Aqueduct, Belmont Park, Keeneland, Santa Anita and others were postponed or cancelled and not running on their regular dates.

The industry should be thankful for the role that ADWs played as almost 100 percent of the wagering in 2020 on these tracks was bet on ADWS.

Having said that, the two smaller tracks listed received the baseline ADW handle payment of three percent, which means that, for every $1 million wagered on these tracks at an ADW, the tracks and their purse accounts each received $15,000.

This is pure speculation on my part, but let’s assume that the other three tracks received a blended rate of five percent, a significant increase over the three percent base rate that would result in a payment of $25,000 each.

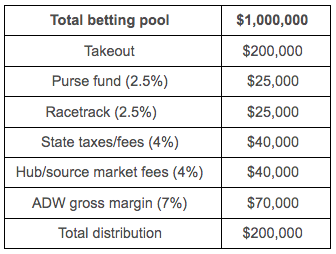

Let’s further assume that the takeout rate for these tracks is a blended 20 percent across all straight and exotic pools. For every $1 million wagered, the takeout pool would be $200,000. Every state has different state taxes/regulatory fees and various hub fees or source market fees. Here is a very theoretical distribution of the $200k takeout per $1 million of an ADW account bet:

Under this model, the ADW gross margin receipts would be 40 percent greater than the total proceeds to the racetrack and the purse account.

By comparison, an on-track bet would result in a payment to the track and the purse account where it would split a range of 8-12 percent of the wagering pool, which would be a range of $80,000-$120,000.

The simple fact and the only intelligent conclusion that one can reach is that the Thoroughbred racing industry is completely in the dark regarding the finances and the true business activities of the ADW companies and their impact on the finances of the industry.

I think the biggest financial issue with ADWs and tracks is the pricing structure that was launched when ADW wagering was initiated in 1999 on the back of simulcast wagering.

Small simulcast fee

At that time, the pricing was viewed as an extension of three percent simulcast fees, where the ADW and the simulcast customer were not impinging on the home market of the racetrack. That small simulcast or ADW fee would be split between the host track and its purse account and considered as ancillary revenue, and the ADW would collect a disproportionate share of the wager from that non-competitive customer.

Unfortunately, today that customer, who was once thought by the track to be a non-competitive customer when ADWs and simulcasting were introduced, now could very well be sitting in a track’s grandstand or wagering online at home in close proximity to the track while returning to the local track a small percentage of their local wager.

Years ago, I had a meeting in my office with the top executive of one of the major ADW companies at Saratoga right after the Jockey Club Round Table conference. This fellow had already worked himself up a bit.

In a somewhat angry and loud voice, he said to me, “I am paying NYRA too much for your signal.” I paused, shook my head thoughtfully and said, “If you really and truly believe that, then you simply should not buy the NYRA signal.”

He paused and then stormed out of my office. The topic never came up again. Perhaps it is time for someone to have a similar conversation.