When the Covid-19 pandemic arrived full blown in New York City in March last year, it became clear that we were in for a very serious health crisis, the likes of which I certainly had not seen in my lifetime.

My wife, Betsy Senior, had to close her art gallery and, by the end of the month, we had packed up our car and, along with our 18- and 19-year old cats, drove to Saratoga Springs. We have been here ever since, with the occasional trip back to New York City, which bears no resemblance to the NYC that we have known for the last 20 years.

By early April, I recall thinking that racing was in for a freefall with only five tracks running: Gulfstream Park, Tampa Bay Downs, Oaklawn Park, Fonner Park and Will Rogers Downs. Remarkably for the month of April 2020, these five tracks had a handle increase of 269 percent over April 2019 and were only nine percent lower than the top ten tracks that ran in April 2019. It was difficult to get too excited as a lot of tracks were still not operating, but it was encouraging.

However, all professional sports had suspended their seasons so there was no competition from other sports on television. Fortunately, led by NYRA, the Jockey Club and Breeders’ Cup and others, America’s Day at the Races was broadcasting races from NYRA, Gulfstream, Churchill and other regional tracks on Fox Sports with some regional TV broadcasts on MSG.

TVG did a deal with NBCSN to run a number of their major tracks on the NBCSN network. Both television deals continued to the end of 2020, and the wagering activity and ratings were strong.

Tony Allevato, NYRA Bets President and Chief Revenue Officer, told Bob Ehalt in a Blood-Horse interview, “It was amazing what our team, and horseracing in general, accomplished by keeping the sport going when other sports couldn’t carry on and by producing so many hours of television coverage under difficult conditions.”

Remarkably, the wagering numbers held up through the end of 2020 despite most tracks being unable to admit any customers.

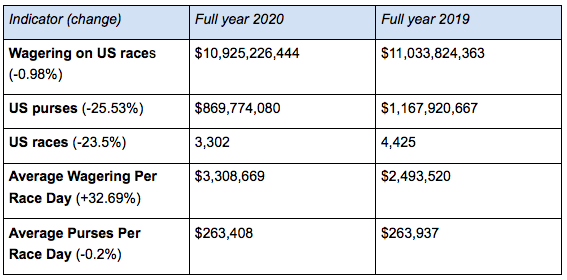

Comparisons: 2020 vs 2019

In reviewing the numbers, it is remarkable that despite running 23.5 percent fewer races, the total handle for the year was down less than one percent. Purses were down 25.53 percent, which is consistent with a reduction in races by 23.5 percent.

The most surprising number for me was the increase in Average Wagering Per Race Day by 32.69 percent. Clearly the increase in hours of television on Fox and NBCSN was important for racing. NYRA and Fox Sports increased the number of televised hours from 385 in 2019 to 777.5 hours in 2020.

There is no way to measure any increase in new customers, but the account wagering companies have indicated that a number of the new customers signed up for an ADW account. They made multiple new deposits, which would seem to indicate that ADWs have kept some of the new business.

Clearly, there has been a substantial increase in ADW market share in 2020. While there have not been any year-end financials published by the ADWs, there have been some strong indications from a few tracks regarding the growth of ADW during this pandemic.

Increasing concerns

Greg Avioli, President of the Thoroughbred Owners of California (TOC), announced that ADW business in California had increased in 2020 to $1 billion, up from $600 million in 2019, or an increase of approximately 67 percent. In 2019, Saratoga set a new handle record of $705+ million and in 2020 the Saratoga handle was just $3 million short of that. I would have to speculate that the Saratoga 2020 ADW handle was well over 60 percent of that, and perhaps double the 2019 ADW handle.

As the racing calendar moved into the summer season, it was great to see that total handle around the U.S. was relatively strong. However, I was increasingly concerned about the implications that this strong reliance the industry had on ADW revenue would have on related payments to tracks and purses.

My concern was amplified by an excellent column from the Thoroughbred Idea Foundation on July 31 titled Racing Not Only for (The) Elite. (Although no author was cited, I presume it was written by their Executive Director, Pat Cummings, who is very knowledgeable on this topic.)

If you are an owner, a bettor or work anywhere in the Thoroughbred racing industry, this is essential reading. This quote from the article particularly deserves your attention:

The disparity between HVBS customers [this is TIF’s acronym for High-Volume Betting Shop] and all others has grown in the last 16 years, but again specific details never seem to be forthcoming from tracks or understood by the groups representing horsepeople. We are left to estimate market size.

A situation where one segment of customers are winning at incredibly high rates and another losing at incredibly high rates has a long-term, destructive effect on losers- notably, they stop playing.

Racing both wants and needs the handle from all players, but the actions of the business-side of the sport, in concert with the general ignorance from the representative groups of horsepeople and major industry organizations, has contributed to this decline of non-high-volume players.

Groundbreaking report

A simple example of a way to demonstrate what is at work here is that total purses paid on U.S. races peaked in 2003 at $15.18 million and, for 2020, total purses were $10,925 million for a decline of 28 percent. HVBS and computer-assisted wagerers (CRW) and the ADW businesses were just getting started around 2000 and their businesses have grown dramatically, while the handle of brick-and-mortar tracks and their OTB outlets has declined.

The TIF article recommends a groundbreaking report, Declining Purses and Track Commissions in Thoroughbred Racing: Causes and Solutions, produced by the NTRA Wagering Systems Task Force in September 2004.

The task force chairman was NTRA President Greg Avioli and there were 30 senior racing industry executives - see page 2 of the report. The NTRA retained the NERA Economic Group to assist in the research and preparation of the final report.

As TIF points out, the final report was over 100 pages, including exhibits, and had significant insights and recommendations.

Chapter 2 of the report was titled Handle Up, Revenue (and Purses) Down: An Economic Analysis of Current Trends in the Thoroughbred Racing Industry. It is important to remember that the CRW, rebaters, HVBS customers etc, according to this report, wagered around $1.2 billion in 2003. Please keep in mind that Illinois was the first state to legalize internet wagering in 1999 and total internet wagering on racing in 2000 was $200 million. So the total ADW revenue would not have had a significant impact on the regular track customers in 2002-2003.

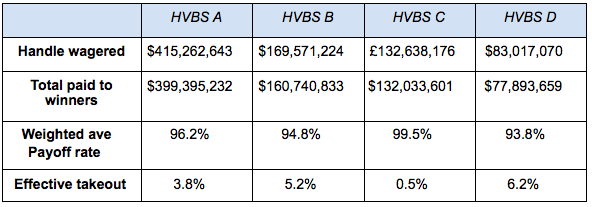

The task force organized 17 tracks and six HVBS/CRW customers to share their total wagers (handle), the winning payouts from the tracks and the weighted average payoff rate. Here are the results. Please note that this is not the total populations of tracks and HVBS/CRWs, and I have included the four largest HVBS sites that participated.

Please note that this is before the rebate from the tracks, which probably would have averaged 5-10 percent of the handle depending on the volume of the HVBS

Coincidentally, I joined NYRA in November 2004. Soon after, we conducted a review of the performance of the six rebaters with whom NYRA did business for the 36-day 2004 Saratoga meeting. Our total Saratoga 2004 handle was $550 million, the rebaters wagered $50 million and NYRA returned $51 million. The takeout rate for the remaining customers was effectively two percent higher. This was a low number due to NYRA not allowing certain rebaters to bet at Saratoga.

In the NTRA Task Force report on these 17 tracks, it was reported that, on WPS wagers, the effective takeout was at least 2.5 percentage points higher and, on daily double/exacta/exotic bets, the affective takeout on the non-rebated customer had a 3.5-4 percent higher takeout than the track’s nominal takeout rate.

The Thoroughbred racing industry has a very high takeout rate at 20-plus percent, especially when you consider that sports betting became legal in May 2018 and has a takeout rate of 5-6 percent depending on the bet.

When you consider that CRW wagering volume could be as high as $2 billion in the U.S. alone, the effective takeout for the average bettor is clearly driving people out of the sport.

Before we leave the task force report, I strongly suggest you take a few minutes go to Chapter 3, which is only two pages and has proposed recommendations on:

- Economic Analysis

- Technology

- Integrity

- Betting Exchange/Bookmakers

- Legislative/Regulatory

Sixteen-plus years have passed since the report was issued, but there are still a number of recommendations that could improve the transparency and understanding of the account wagering/rebate business for all racing industry participants. Again, a lot of very good work was done on this as you will see, but most of the problems that were raised remain today.

Below is a quote from Curtis Linnell, Executive VP of the Thoroughbred Racing Protective Bureau, whose mandate is to provide integrity analysis and security services for TRA racetrack wagering networks and contracted associations/agencies. No-one in Thoroughbred racing knows more about wagering security and the finances of ADWs and all aspects of account wagering, including CRW, than Linnell. This quote appeared in a Frank Angst article in The Blood-Horse after an ARCI conference in March, 2016:

Linnell noted that nearly $5 billion has disappeared from Thoroughbred pari-mutuel pools since 2002, a trend that might lead many businesses to look at their pricing structure. But, instead of lowering its takeout for all players, which would be a more attractive model to new- and medium-level horseplayers, the industry has taken the approach of rebating its very top players. That approach means that tracks receive less benefit from every dollar wagered by these players.

The following comment appeared underneath the article and is from Paul Berube, President for 17 years of the Thoroughbred Racing Protective Bureau.

“Curtis Linnell is the most brilliant operational mind in pari-mutuel racing today ... A corollary to his remarks is that, when CRW (computer robotic wagering) teams win, they do not churn back their winnings as regular players do. Instead they remain disciplined by betting only to the ‘value’ perceived by their programs and to pool totals established by all other players. Because CRW winning bets tend to lower payoffs, regular players who win on the same bets have less money to churn. Ergo less money to bet translates to smaller pools and declining pari-mutuel handle overall.

"A reasonable conclusion is that computer teams are and always have been a long-term negative for racing’s pari-mutuel business. Pricing the simulcast product so that rebates can be given to this destructive form of wagering is just short of insane. Where will this lead to in another 5-10 years? No where good I suspect.”

Where we are on ADWs

Now a brief review the background of Advanced Deposit Wagering and a look at where I believe we find ourselves today.

As I noted above, the very first U.S. state to legalize internet wagering on horseracing was Illinois in 1999 with total internet wagering in 2000 at $200 million. One of the early pioneers of ADW wagering was Charlie Ruma, who owned Beulah Downs and River Downs, and launched America Tab and was able to acquire content from most of the major tracks that he had simulcasting deals with at the standard rate of three percent. Almost all deals done in the early days of simulcasting were for three percent as racetracks looked at it as an extension of their business outside their market with little incremental cost. Unfortunately, many ADW deals today are still done at three percent and very few deals are done above six percent.

Fonner Park in Nebraska had always run a four-week meeting. In 2020, it was one of only five tracks racing during the month of April. As a result, while Fonner had averaged a daily handle of $600,000 in previous years, its average in 2020 was $3.6 million at the three-percent rate. This meant for every $2 million of ADW handle (Fonner had no live attendance), the track received $30,000 and the purse account the same.

When Chris Kotulak, CEO of Fonner, applied for an additional four weeks of racing in May, he received a signal increase to five percent for his additional four weeks, but only if he agreed to go back to three percent for 2021. Despite the significant growth of the ADW business in the last two decades, there are today more deals done closer to three percent than six percent.

Moves by Churchill Downs

Recognizing the low operating cost and reasonable capital costs of an ADW (as compared to a racetrack), Churchill Downs launched Twin Spires just before the Kentucky Derby in May 2007. It had a successful sign-up launch and, within the next two months, in two separate deals Churchill bought AmericaTab, Bloodstock Research, including BrisBet, and Thoroughbred Sports Network (TSN).

A little over two years later, Churchill bought both youbet.com and one of three American tote companies, United Tote. While Churchill was very actively acquiring ADW properties, it sold off a number of racetrack assets.

It had purchased Hollywood Park in September 1999 and sold it to a land management company in 2005. Churchill leased its racing property on the grounds of its Calder Casino in Miami to the Stronach Group, which recently closed the track when the lease ran out. In July 2020, Churchill announced its plan to sell Arlington Park sometime in the future.

Churchill was clearly making some good business decisions as its stock has increased almost exactly 150 percent over the last three years. This also is a pretty clear indication that owning and operating an ADW has stronger profitable attributes with much less operating expense and capital costs. Twin Spires is currently the second largest ADW in the U.S.

The largest (not counting CRW businesses) is TVG, which was launched in 1999 and sold to Betfair in January 2009 and is now part of the Flutter Entertainment Group.

Rounding out the top four ADWs in the U.S. are Xpress, owned by the Stronach Group and founded in 2002, and NYRABets, which was launched as an internet ADW in 2007.

In the dark

The simple fact and the only intelligent conclusion that one can reach is that the Thoroughbred racing industry is completely in the dark regarding the finances and the true business activities of both the Computer Robotic Wagering companies and the Advanced Deposit Wagering companies and their impact on the finances of the industry.

Let’s discuss the CRW situation first.

The industry knows virtually nothing about the operations and finances of CRW companies. Innocently, I recently asked a track executive why Elite Turf Club was not on a state’s list of companies that takes bets from that state’s residents for the calculation of the state’s source market fee. Interestingly, the executive explained that it is a non-U.S. company based in Curacao in the Caribbean.

Really. I believe it is owned by the Stronach Group. They have around 20 separate CRW teams, many of which are U.S. citizens.

Why is there no public report on how much dollar volume in handle it is generating, and what its ‘effective’ or actual takeout rate is?

In a 2003 report - the most recent one as I sit here in 2021 that the industry has on four CRW operators - the actual, ‘effective’ takeout rates were not anywhere near the posted rate. The CRW operators from that 2003 study were paying a takeout of from 0.5 percent to six percent on handle, and that is before the hundreds of thousands of dollars in rebates that the industry is paying these CRM operators.

Undermining our finances?

There is some speculation online that Elite could be wagering $1 billion dollars annually into the pools of American racetracks. There is also speculation, but no facts, that on straight bets the ‘regular’ customer could be paying an additional 2-3percent on straight bets and possibly 3-5 percent on doubles, exactas and exotic bets.

The track management should have the power to operate the track in the most professional manner it deems appropriate. The management has to be accountable ultimately to the owners, breeders, employees, customers and members of their community.

My personal opinion, based on experience, research, and well-informed professionals, suggests that the CRM companies are paying the U.S. racing industry money in the form of handle that is undermining the finances of our core business.

There are two huge distinct advantages that the Computer Robotic Wagerer has over the regular player who is betting into the pool the old fashioned way (ie, with a teller, at a tote machine or even with a bettor’s own computer). The robotic player has direct access to the track/host tote pool, which gives them at least two huge competitive advantages:

- They can scan directly into the host pool and compare the value of horses in straight betting pools with the detailed calculation that their computer analyst(s) have done for each horse in the race and wager accordingly.

- They can then wait and make thousands of bets in the last minute(s) before the pools close. This would be the equivalent of a CRW player sitting at a poker table in Vegas and before the last final round of bets are made, being allowed to look at all the cards of the other players at the table and to make his final bet in this round.

I think that this would be particularly valuable in the Jackpot Pick 6 bets where the bet does not pay off if more than one bettor hits the Pick 6. A modest consolation payoff is made to the multiple winners and the rest of the pool carries over to the next day of racing. Once the pot builds up to a six- or seven-figure pot, the CRW player has the liquidity and the information to take down the pot alone. If the track reports who took down the Jackpot Pick (and many don’t) in the U.S., you will often see Elite Turf Club as the winner. However, the CRW has a distinct advantage of scanning the pools and placing the bet at the very last minute for all types of wagers: WPS, Daily Double, Exacta and other exotics, pick 3, 4, 5, etc.

The CRM teams are talented, well informed with strong liquidity. but they should not have these unfair advantages.

Lack of transparency

Turning to the ADWs, there are some similar concerns that I have regarding the lack of transparency with U.S. ADW operations.

Shame on me, but when I was at NYRA from the time that we launched NYRA Rewards (which became NYRA Bets), I never initiated a request for an audit of an ADW that sold the NYRA racing product, nor did we have any audit request from a racetrack of the NYRA Bets operation before I left the association in 2012.

That is simply unacceptable. Regular audits should be part of any executed contract.

When I was at NYRA, we published our detailed financial statements monthly and, given our financial situation and history, it was not a pleasant exercise. But we were held accountable and answered any questions to the best of our knowledge. NYRA eliminated all financial reporting on its website. In fact the headings are still on the website now, with no data.

Also, the state-by-state source-market fees are a morass and a nightmare. Source-market fees arose once national ADWs could market betting on their tracks nationally. The concept of the source-market fee was intended to protect the local track within a certain radius from ADWs coming in and marketing to the track’s customers.

Unfortunately, the source-market fee varied from track to track and state to state. Some customer recruiters from an ADW would offer a client bettor an actual address in another state which they could use to reduce their source-market fees costs. If this is still going on, it has to stop - and it can be stopped by regular audits.

Biggest issue

I think the biggest financial issue with ADWs and tracks is the pricing structure that was launched when ADW pricing was launched. At that time, the pricing was viewed as an extension of 3 percent simulcast fees, where that fee would be split between the host track and its purse account, and the ADW would collect a disproportionate size of the bet.

Look, the historical perspective is simple to understand, but the logic of the pricing has to address the real costs of conducting a race meet versus the relatively small marginal cost of running an ADW.

For example, at Saratoga, NYRA runs a 40-day meet where there is a main track with a dirt track and two turf courses and a training track with a dirt course, a pony track and a turf course, 1,200 stalls, 1,000 dorm rooms and training that runs from mid-April to late October, plus the 1,500 employees for the meet itself.

I truly believe that the people who participate in the racing and breeding programs and the people who make the business go, including the employees, the bettors and all the others truly care about the future of the industry. However, to be successful, everyone has to get on the same team and every racing industry participant has a right to know how their part of the industry operates and what they are expected to do to make it better. An update to the detailed NTRA report of 2004 is long overdue.

Somehow, I think that, if a CRM operator built a better program for betting on Swedish harness races, Irish football, Italian soccer, American tennis etc, they would move their business immediately.

American racing should not be run to give bettors a bigger and better economic incentive but rather to focus on the needs and concerns of our racing participants, customers, owners and breeders. I am certainly prepared to do my part to move the industry forward. Where do we sign up?