In his regular column, Charles Hayward says it’s time to face up to a serious problem besetting the racing industry’s economic model amid a changing betting environment in th wake of Covid-19

The racing industry should be thankful for the role that role that the Advanced Deposit Wagering (ADW) companies played during the pandemic as almost 100% of US wagering in 2020 on horse racing was bet via ADWs.

The majority of racetracks that were racing in 2020 were behind closed doors, not allowing customers due to the pandemic.

However, as these account-wagering businesses have grown, the current economic model strongly favors them at the expense of on-track handle, which returns much more to horse racing.

Twin Spires and TVG are dominant forces

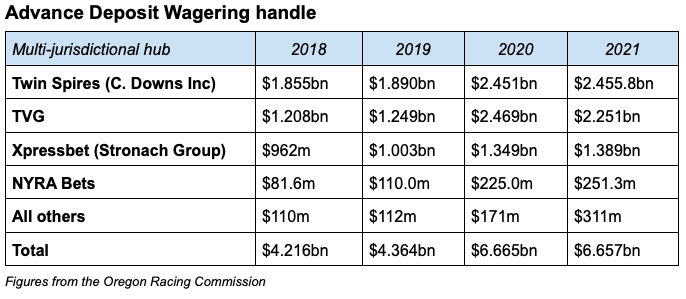

Through the end of 2021, the ADW sector is dominated by two companies: Twin Spires, owned by Louisville-based Churchill Downs Inc., and Television Games Network (TVG) based in Los Angeles and part of the Flutter Entertainment Group, whose HQ is in Dublin.

As of December 2021, on their own those two companies controlled a massive 71% of the US ADW market. While TVG operates a much respected racing broadcast channel, Flutter is a large gaming and betting corporation with no other links to the horse racing industry and Churchill Downs Inc. is also clearly a strong gaming company and their recent actions – selling off Arlington Park and ending racing at Bay Meadows, Hollywood Park and Calder – suggest motives other than the promotion of the sport.

Admittedly, Churchill Downs Inc. still maintains some valuable racing assets such as Churchill Downs itself – the home of the Kentucky Derby – but any tracks they have purchased recently were acquired on account of their casino/gaming businesses.

Two other serious ADW operators have greater racing involvement. New York Racing Association (NYRA) operates Saratoga, Belmont Park and Aqueduct, while the Stronach Group (who operate the ADW brand Xpressbet) possess strong assets in Santa Anita, Gulfstream Park and several other racetracks and training centers.

In the interests of full disclosure, here I should remind readers that I am a former president of NYRA. Be that as it may, from the outset, NYRA has been the most progressive company for the benefit of the racing industry.

For example, when the internet ADW business was launched strictly in the state of New York, NYRA BETS was the only racing company to pay horse owners the purse amount equivalent to a live track race rather than a small slice of the ADW fee which was standard industry practice.

By 2018, NYRA negotiated a national television contract resulting in over 700 hours of NYRA races in prominent markets across the country. In 2020, NYRA announced that they had sold a 25% interest in NYRA BETS to Fox Sports.

Looking back, as the ADW business model evolved in the 1999, racetracks viewed most ADW operators as a plus – basically, incremental business – so almost all tracks started out selling their signal for only 3% of the wager that the track split with horse owners.

Economic model slow to adjust

Well, computers and the Interstate Horseracing Act changed all that – but the economic model has been very slow to adjust to a fair market rate for the track’s races. The result is that the account wagering company makes a larger percentage of the wager than the racetrack and horse owners combined.

Having said that, the track and their purse account on many occasions receive an ADW handle payment of 5% of the wager, which means that, for every $1m bet on these tracks at an ADW, the tracks and their purse accounts each received $25,000.

Yet nevertheless, in most instances the ADW operator will receive more than the combined payment to the track and the purse account.

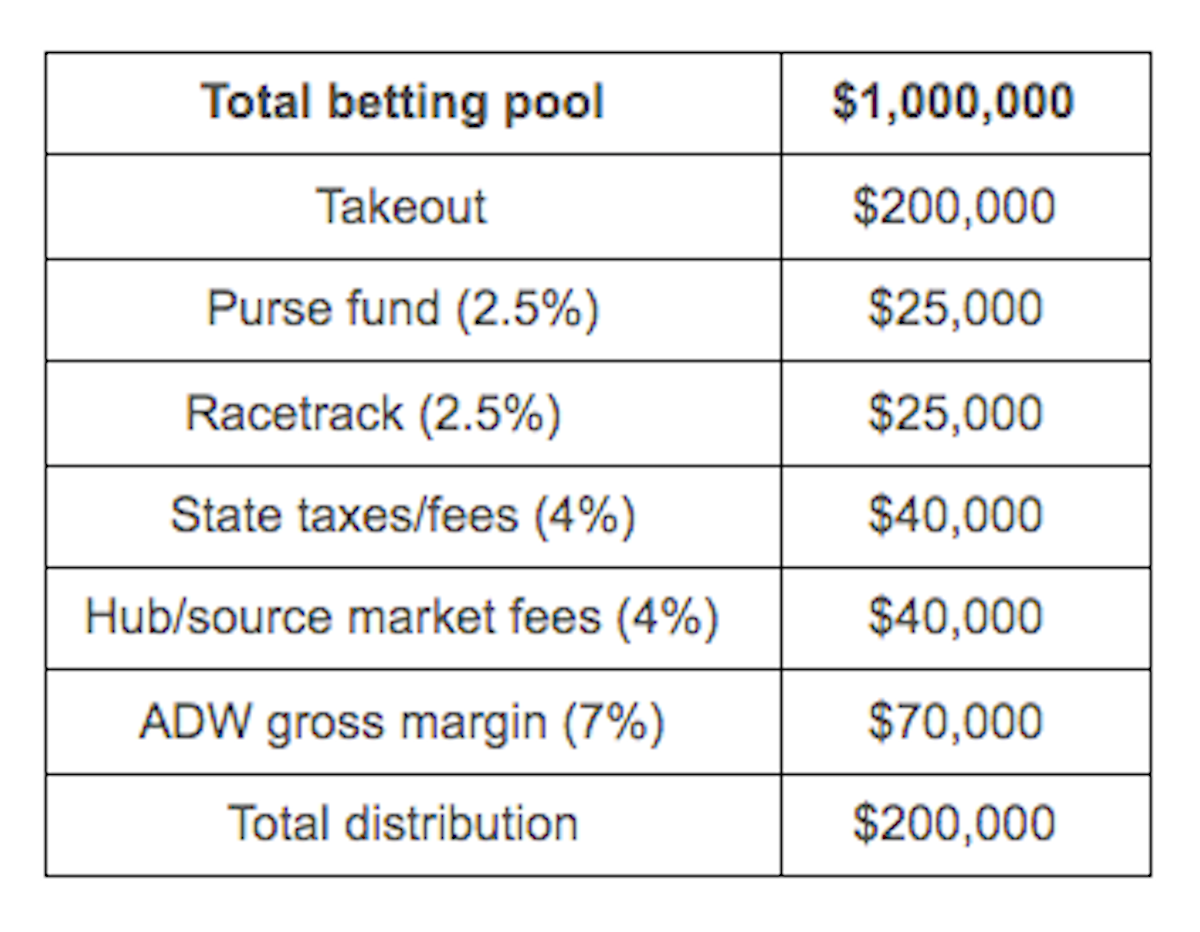

Look at this pro forma model. Let’s assume that the takeout rate for these tracks is a blended 20% across all straight and exotic pools. For every $1m wagered, the takeout pool would be $200,000. Every state has different state taxes/regulatory fees and various hub fees or source market fees but here is a very theoretical distribution of the $200k takeout per $1m of ADW account wagers.

Look at this pro forma model. Let’s assume that the takeout rate for these tracks is a blended 20% across all straight and exotic pools. For every $1m wagered, the takeout pool would be $200,000. Every state has different state taxes/regulatory fees and various hub fees or source market fees but here is a very theoretical distribution of the $200k takeout per $1m of ADW account wagers.

Under this model, the ADW gross margin receipts would be 40% greater than the total proceeds to the racetrack and the purse account. By comparison, an on-track bet would result in a payment to the track and the purse account where it would split a range of 8-12% of the pool, which would be a range of $80,000-$120,000.

The simple fact – indeed, the only intelligent conclusion one can reach – is that the Thoroughbred racing industry is completely in the dark regarding the finances and the true business activities of ADW companies and their impact on the finances of the industry.

Serious strategic and financial issue

The Thoroughbred racing industry faces a serious strategic and financial issue. As we have seen, the two companies that represent 70%-plus of the ADW sales, Churchill Downs Inc. and TVG, are powerful gaming companies.

TVG has no real racing assets; Churchill Downs has control over the Kentucky Derby meet and places like Turfway Park, Presque Isle and Colonial Downs, but in light of what happened at Arlington and elsewhere, their stewardship is hardly designed to inspire massive confidence among the racing community.

With all that in mind, I think the biggest financial issue with ADWs and tracks is the pricing structure that was launched when ADW wagering was initiated in 1999 on the back of simulcast wagering.

Small simulcast fee

At that time, the pricing was viewed as an extension of 3% simulcast fees, where the ADW and the simulcast customer were not impinging on the racetrack’s home market. That small simulcast or ADW fee would be split between the host track and its purse account and considered as ancillary revenue, and the ADW would collect adisproportionate share of the wager from what was then considered a non-competitive customer.

Unfortunately, nowadays that customer could very well be sitting in the track’s grandstand or wagering online at home in close proximity to the track. They are now clearly a competitive entity who might otherwise be wagering on-track and returning more to the sport.

Years ago, I had a meeting in my office at NYRA with the top executive of one of the major ADW companies at Saratoga after the annual Jockey Club Round Table conference. This fellow had already worked himself up a bit. In a somewhat angry and loud voice, he said to me: “I am paying NYRA too much for your signal.”

I paused, shook my head thoughtfully, and said: “If you really and truly believe that, then you simply should not buy the NYRA signal.”

He paused and then stormed out of my office. The topic never came up again. Perhaps it is time for many track operators to have similar conversations with their ADW vendors.

Jay Hovdey's Favorite Racehorses: Ancient Title – ‘There were so many times he took the breath away’

Charles Hayward: Change the culture – or risk going the way of the circus and dog racing

Charles Hayward: If we don’t clean up our act, we won’t have a sport

View the latest TRC Global Rankings for horses / jockeys / trainers / sires